You need a deposit

There’s no two ways about it; when you’re looking at buying your first home you will need some kind of deposit! At the very minimum you will need 10% - 20% of the purchase price as a deposit. For many people the prospect of having to save a minimum of $60,000 - $150,000 is enough to make them kiss their home ownership dreams goodbye. With a bit of planning and commitment, you can get that deposit together and it doesn’t all have to come from squirreling away!...Here’s where you can pull it all together.

Saving

Saving is an important piece to the puzzle. The obvious thing here is to setup a budget. What is your income vs expenses and figure out what you can afford to put into savings. The idea here is to slowly put together a chunk for your deposit and to show the bank that you are capable of saving money and are disciplined with it. This savings history will definitely help with getting your pre-approval.

Kiwisaver

Most first home buyers are going to rely on their Kiwisaver funds to purchase their new home. It’s incredibly valuable to sign up for Kiwisaver if you want to buy your first home. Not only do you contribute to Kiwisaver, but your employer and even the government does. It’s money-for-nothing and you’d be surprised how quickly the funds can add up, especially if you are buying a house with your partner and have two lots of Kiwisaver to contribute.

It’s worth considering making higher contributions to Kiwisaver if you think you will struggle to be disciplined enough to make savings. Consider increasing your contribution from the minimum 3% to 4% or if your budget allows, 8%. This will speed things up for you!

It’s important to know what kind of fund you are in and with which provider. If you do not specify a provider when signing up for Kiwisaver, the IRD will randomly choose one. It’s best to know where it is and in what type of fund so that you can make informed decisions around how that money is invested. We would recommend seeking financial advice to ensure you are in the best fund to help you achieve your goals.

Kiwisaver is an awesome tool for first home buyers and can make a real impact if you have been in the scheme for a decent amount of time. Remember, you can’t touch the money unless you want to buy your first home with it.

Government help

The First Home Grant is money from Kainga Ora to assist you with your deposit to purchase a property.

You can receive between $3K - $5K for an existing property and between $6K - $10K for new homes depending on how long you've been contributing to KiwiSaver (3, 4 or 5 + years).

This money is non-repayable, but there are a few boxes to tick, so check out our guide for the criteria you'll need to meet alongside the KiwiSaver criteria above:

✓ Earn under the income threshold of $95K for an individual or $150K for a couple

✓ Be a permanent New Zealand resident with no visa travel conditions or an NZ Citizen

✓ Have at least 5% deposit

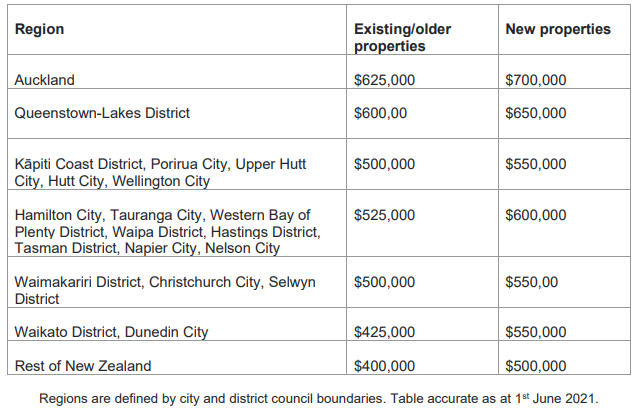

✓ Meet the house price caps for your region (see table below or resources with link to updated table)

The First Home Grant goes alongside the First Home Loan scheme also backed by Kainga Ora. Requirements are similar to the grant and additionally need to show stable employment in your role or industry for at least 12 months. This is a scheme to help first home buyers with a low deposit into their first home. A select number of banks offer this product so you can check in with us on who these are and if it is an option for you.

Gifting

If you’re really lucky you may be gifted some money towards your deposit from a family member. This can definitely be used towards your deposit. It’s best to talk to a mortgage advisor about the gift so that the right documentation can be arranged to include this gift as part of your deposit.

Other tips to get your deposit together...

Reduce living costs, increase income

Easier said than done, we know, but reducing your living costs and increasing your income can speed up the process of saving for your first home.

You can decrease your living costs by living with other people, living with your family or moving into a flat. Change your spending habits...do you really need that Netflix account? Short term pain, for long term gain is the idea here.

Think about the ways you can increase your income. Perhaps the opportunity is there to work a few more hours or you could try looking for some kind of side hustle. Heck, mow the neighbours lawn! Put any extra income you receive directly into your savings.

Set a budget!

The most important thing in getting to your goal is that you set yourself up with a budget. Take a really hard look at what your income is versus your expenses. What do you have leftover to put into savings?

From here, work out how long it’s going to take you to get to where you need to be to buy a house. It may be 6 months away or 3 years away but to get there, you will absolutely need a budget and stick to it.

Budgeting Help

- Check out Pocketsmith - A nifty little app that will automatically categorise your spending and help you make informed decisions about your spending. It does cost $10 a month, so make sure you will be saving more by using it

- Setup a basic spreadsheet - Setup a column with your weekly or monthly expenses (this may take a little bit of working out by going through bank statements), total it up down the bottom and see how it compares with your income. From here you can look at what you can reduce or remove altogether and how much you can put away. You can google 'budgeting spreadsheets', there are heaps of free downloads.

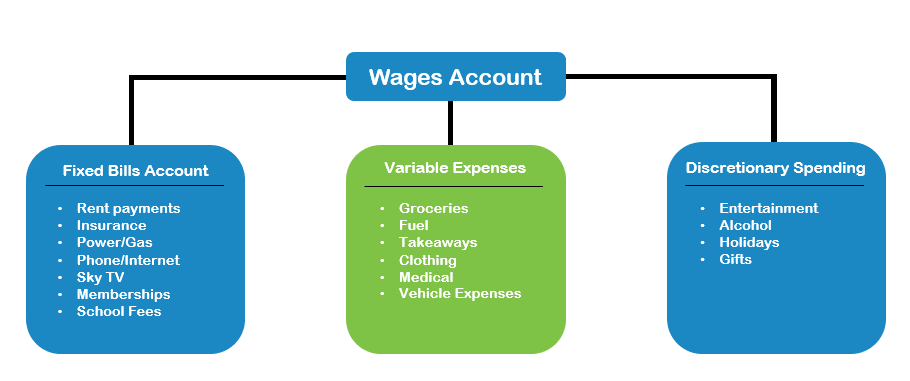

- Setup automatic payments and separate accounts. Try to automate as much as possible, so that you don't spend money you don't have. To help with this, setup different accounts for different purposes.

- Transfer an amount to either an account like the above or another savings account that you can comfortably do every week or pay period. It might be small like $5 initially but the key is to not take funds out of this account. Even if unexpected expenses come along, you are showing the bank you have the ability to set aside and be diligent with money

A good way of setting it up is to have three spending accounts, see the diagram below.

It's not as bad as it sounds!...

Taking a look at how a typical first home buyer's deposit might be made up, may reassure you that you don’t need to just save a huge chunk of money to get the deposit you need.

Let’s say you and a partner were able to save $30,000. You each had $17,000 in your Kiwisaver accounts (the average amount New Zealanders have in their Kiwisaver account) and then you were each to receive a first home grant of $5,000 for an existing property...

Savings: $30,000

Kiwisaver Applicant 1: $17,000

Kiwisaver Applicant 2: $17,000

First Home Grant Applicant 1: $5,000

First Home Grant Applicant 2: $5,000

Your total deposit would be $74,000 which is certainly on the way to being able to buy your first home!

Now that you've got your deposit, you're ready to move onto the next step of your home ownership journey! *woo-hoo!* So who exactly is involved with your next step? Read Part 3: Who's involved in your first home purchase?